Every practice management guide gives you the same benchmarks for utilization rate at an accounting firm. Target 65% to 85% for individual staff. Above 85% burns people out. Below 65% wastes capacity. The number gets quoted like it came from somewhere. Nobody ever tells you where.

Then you look at your own firm. Utilization says 70%. On paper, 30% of the week is free. And your team is still telling you they're drowning.

The 85% number is real. It just isn't measuring what you think it's measuring. What follows traces where the number actually came from, then rebuilds the metric it was supposed to sit on top of.

Key takeaways

- The 85% number is right. The metric it sits on is wrong. The cap has no cited origin in accounting practice management. It does have one in sports coaching, where it applies to total effort with 15% held in reserve, not to billable hours as a share of available hours. Same number, different application.

- A firm at 70% utilization can still be at 100% capacity load. The 30% the utilization dashboard shows as spare is already burning on admin, meetings, tool switching, and chasing clients for signatures and documents. Which is why the dashboard reads fine while the team says they're drowning.

- The 15% under the cap is reserve, not slack. Roughly six hours a week that the person controls, that the firm doesn't schedule against, and that they don't have to justify. Its absence is what makes a fully-booked week feel different from a productive one.

- You can surface capacity load without adding a single time-tracking category. Ask every client-facing person "if you had two extra hours this week, no strings, what would you do?" One-on-one. Unexplained. Recorded verbatim. The friction they name is the friction they're already carrying.

- What people would do with reserve time is what your firm can't currently produce. Quality answers mean errors are landing at clients. Relationship answers mean referrals and calls are dying on the vine. System answers mean the next efficiency gain is blocked. The category of the answer names what the current load is starving.

What the 85% utilization rate rule for accounting firms actually says

The utilization rate for accounting firms is billable hours divided by total available hours, expressed as a percentage. The industry consensus targets 65% to 85% for individual staff and around 60% firm-wide. The 85% ceiling exists to prevent burnout. Above 85%, quality drops and turnover rises. Below 65%, the firm has excess capacity going to waste.

That formula gets repeated in AICPA benchmark surveys, in practice management platforms, and in every time-tracking product's onboarding material. The 65-85% range shows up in the same paragraph as burnout and turnover, and it does its job. Managers know what number to look at. Partners know when to worry.

The reality has been below the range for a while. The 2026 SPI Research Professional Services Maturity Benchmark, based on 509 firms, put professional services billable utilization at 66.4% in 2025, an all-time historic low. CPA Practice Advisor's editorial coverage of the profitability data identifies 70% to 80% as the utilization "sweet spot" for margin health. Most firms are underneath it.

Which raises the question the industry doesn't answer. Why 85%? Not 80. Not 90. The specific number sits as a hard cap in benchmarks and tool defaults across the profession, and nobody who quotes it can source it back to what makes 85 the ceiling.

Where the 85% number actually comes from

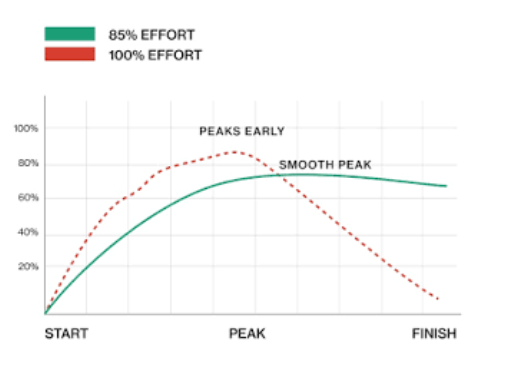

The 85% cap has no cited origin in accounting practice management literature. The same number does show up in a different tradition: sports coaching, specifically the story of sprinter Carl Lewis.

Lewis won four gold medals at the 1984 Los Angeles Olympics: 100 meters, 200 meters, long jump, and the 4×100 relay, matching Jesse Owens's 1936 feat. He went on to win nine Olympic golds in total across four Games. What matters for the 85% story is what we can see on video.

At the 40-meter mark, Lewis was often at the back of the pack. By the last stretch, he had passed everyone. The other runners visibly pushed. Clenched fists, tight jaws, scrunched faces. They also slowed down. Lewis stayed relaxed and kept the same pace. His finishing speed wasn't the result of more effort. It was the result of less tension.

Why? Because human peak performance sit at roughly 85% of maximum effort, not 100%. The runners pushing to 100% weren't running faster than Lewis. They were running against their own body. The extra 15% of effort went into muscles fighting each other, not into forward motion. The insight got named later. Peak sustainable performance sits at roughly 85% of maximum effort, with 15% held in reserve.

The number is the same. The measure it's applied to isn't.

That's a very different definition of 85% than the one accounting uses. The accounting version says 85% of your available hours should go to one specific type of work: billable client work. The sports version says the cap is on total effort of any kind, with 15% held back on purpose. The industry number matches. The thing being measured doesn't.

Why utilization rate is the wrong place to apply the 85% cap

Utilization rate for accounting firms measures billable hours as a share of total available hours. The 85% cap from sports coaching measures total effort as a share of a person's total capacity. Those are different denominators. Applied honestly, the 85% belongs on total capacity load. That means billable work plus admin, meetings, tool switching, and chasing. Not billable share alone.

Capacity load is a total-effort metric. It treats every productive activity going through a person's week as a single load: billable client work, admin blocks, internal meetings, tool switching, chasing clients for documents and signatures, work about the work. All of it counts. The cap of 85% sits on the sum.

Walk through a 40-hour week for a senior accountant at a five-person firm. Twenty-eight hours are billable client work: utilization rate reads 70%, comfortably below the 85% cap, no red flags on the dashboard. Now account for the rest of the week. Three hours of internal meetings and check-ins. Two hours of firm admin, from onboarding forms to internal reporting. Five hours across the week emailing clients for signatures, missing documents, and clarifications on scope. Two hours moving data between the tax software, the practice management platform, and the general ledger. Twelve hours of productive non-billable work, on top of the twenty-eight billable. Total productive load: forty out of forty hours. Capacity load: 100%. Utilization rate still reads 70%.

That 30% the utilization rate showed as spare wasn't spare. It was already booked. The Anatomy of Work Index, which surveyed more than 13,000 knowledge workers globally, found that the average knowledge worker spends 60% of their working time on "work about work": searching for information, chasing approvals, switching between apps, sitting in meetings that could have been an email. Accountants are not exempt. The 2026 Intuit QuickBooks Accountant Technology Survey, which polled 725 US accounting and bookkeeping professionals, found that they lose an average of five hours per week just moving, re-entering, or reconciling data across disconnected systems.

So your utilization rate says 70%. Your capacity load is closer to 100%. That's why your team is drowning.

Firm owners make decisions from the metric they look at. When utilization looks like it has room, firms take on the next client. They defer hiring. They price the new engagement based on billable hours available, not total capacity available. The engagement eats into a reserve that was never there. The metric doesn't register the strain until turnover, missed deadlines, or a lost client makes it visible from another direction.

The 15% the metric leaves below the cap isn't slack. It isn't administrative overhead. It isn't rest. It's reserve, controlled by the person doing the work, available for the mid-race adjustment. On a 40-hour week, that's roughly six hours the person owns. They don't have to justify what they're doing with them, and the firm isn't scheduling anything into them. It's the part of the sprint Lewis had that the other runners had already spent.

How to test capacity load in your firm

To test whether your firm is running above 85% capacity load, ask every client-facing person the same question in a one-on-one setting: "If you had two extra hours this week, no strings, what would you do with them?" Then give one person those two hours the following week and see what they actually choose to do.

The mechanism is a documented experiment you can run this month. The questions are simple. The rules are not. Here is the sequence.

- Ask every client-facing person the same question in a one-on-one. In a group, people perform for the room and give you the answer they think you want to hear. One-on-one, they give you the friction they're actually feeling. Ask everyone who touches a client, not just the senior staff or the people you already trust. You're collecting a pattern, not managing feelings.

- Don't explain why you're asking. The framing contaminates the answer. If you say "I want to give you some free time," they'll optimize for keeping that offer alive rather than tell you what they'd actually do. Record their words as close to verbatim as you can. Don't respond in the moment.

- Look at the pattern across answers. Three categories tend to emerge. Quality answers ("I'd review that return before sending it, I'd proofread the email I sent too fast"): the last 15% is compressing your quality. Relationship answers ("I'd call the client I keep meaning to reach, I'd follow up on that referral"): the last 15% is starving your client trust. System answers ("I'd document that process, I'd fix that workflow that keeps breaking"): the last 15% is blocking your next efficiency gain.

One thread runs through almost every answer sheet regardless of firm: the chasing. Someone always mentions the follow-up loop of signatures, missing documents, payment information, and scope clarifications that eats hours a week per person. If chasing clients is a meaningful portion of your team's capacity load, agreement-first billing removes the whole category. When the payment method is captured at the moment the proposal is signed and billing runs from the agreement, the follow-up loop doesn't need to exist inside anyone's week.

- Pick the answer that surprised you, not the one you agreed with. The surprise is the signal. Give that person two protected hours next week for exactly what they said they'd do. Cover their other work. Don't backfill the two hours with a new task if they finish early. That recreates the 100% capacity load in different packaging.

- If the signal holds, make it permanent for that person for 90 days. Same two hours, same time, same protection. After 90 days you can quantify the value in dollars, in retained clients, or in owner time recovered. If it works there, expand to every client-facing person.

What changes when you measure capacity load instead

A firm that treats 85% as a cap on total capacity load rather than a target for utilization rate changes three things. It stops counting non-billable hours as available time. It builds a real 15% reserve into every client-facing person's week. And it can name what the reserve is producing: quality catches, retained relationships, or documented systems.

One accounting firm that acted on a version of this pattern is Whalen & Company CPAs in Worthington, Ohio. In early 2024, the firm's Managing Partner Lisa Shuneson told Inside Public Accounting that all 35 staff could choose to work no more than 40 hours per week. Everyone kept their full market-rate annual salary regardless of hours chosen. Overtime above 40 was compensated hourly. Every October, staff picked their "all-in" total hours for the coming year, with different percentages marked as billable based on skills and role.

"I'm a realist," Shuneson told the publication. "I feel like you have to address the issues that you get when you try to recruit someone into public accounting, and most of the time the issue is hours."

The firm sustains a $7.1 million revenue business under this structure. That is what capacity load looks like when a firm reorganizes around it rather than around utilization rate. Nobody is staring at a utilization number. Everyone has a defined boundary between the hours they've chosen and the hours they haven't. Recruiting improves for the same reason retention does: the load is legible.

The 15% isn't a luxury. It isn't rest time or recovery time or slack. It's the part of your firm's capacity that produces the work you can't schedule: the review that catches the error, the follow-up call that keeps the client, the process that saves 40 hours next quarter.

_____________________________________________________________________

The 85% number was never wrong. The industry just put it on the wrong denominator. The firms running well aren't hitting a higher utilization rate. They're protecting the 15% the metric never told them to protect.

Out of Scope is our Lunch & Learn series for accounting firm owners. Watch the recording of this session here, or sign up for the next session here.

Common questions about utilization rate and capacity load

What's the difference between utilization rate and capacity load?

Utilization rate measures billable hours as a share of total available hours. Capacity load measures every productive activity as a share of a person's total capacity. That includes billable client work, admin, internal meetings, tool switching, chasing clients, and work about the work. Both use 85% as a benchmark. They measure different denominators. A firm at 70% utilization can still be at 100% capacity load, which is the pattern most owner-operators are actually feeling when the metric on the dashboard doesn't match the mood in the office.

Can I calculate capacity load with the time tracking my firm already uses?

Partially. Existing time tracking captures billable hours cleanly. To calculate capacity load you also need the non-billable productive hours: admin blocks, internal meetings, chasing, tool switching. Most small firms find the fastest path is qualitative rather than quantitative. The two-hour experiment described above surfaces the answer without asking anyone to log every minute of their week. If you want quantitative rigor later, you can add category-level time tracking to non-billable blocks. The signal usually shows up long before the spreadsheet does.

Does the 85% capacity load cap apply during tax season?

Sustained above 85% is unsustainable. Some firms hit 90-95% during peak weeks, and that's expected. The signal isn't the peak. It's whether the average returns below 85% during the recovery months. If your firm-wide capacity load averages above 85% across a full year, tax season isn't the cause. It's a symptom that shows up on a predictable schedule. The firms that come out of April in better shape than they went in aren't running lower peak weeks. They're running lower baselines the other ten months.

Does capacity load apply to solo firms?

Especially to solo firms. A solo owner is running client work, admin, meetings, tool switching, and chasing all on one calendar. The 85% cap on capacity load for a solo practitioner is roughly 34 hours of productive work in a 40-hour week, with 6 hours held in reserve. If that sounds impossible, the reserve is what your firm is currently starving to keep the lights on. Solo firms also have the added trap of no one to redistribute work to when capacity load spikes, which makes the reserve more valuable, not less.