Are you still doing client work all day and then trying to “figure out succession” at night?

In a recent Anchor-hosted webinar, Steve Shein, CFA, co-founder at Franklin Alliance, laid out why firm sales feel louder than ever, and why many owners get surprised by the terms, not the price.

The main insight is clear: you have more options than you think, but you also have more ways to get boxed into a deal that doesn’t align with what you want next.

Keep reading as we turn that conversation into a practical guide you can use before you take serious buyer calls.

Key takeaways

- Optimize for confidence, not just a headline multiple: Buyers are pricing the risk of what happens after you step back, so clean operations and a smooth relationship transition often matter as much as revenue.

- Choose a buyer based on tradeoffs you can live with: Traditional firms, PE-backed platforms, individual buyers, and operating partners can all be “right,” but each comes with a different mix of control, culture change, payout structure, and upside.

- Avoid the late-stage exit trap: The longer you wait to plan the transition, the more your payout can shift into deferred payments tied to collections and retention you may not control post-close.

- Make billing and delivery predictable before you go to market: When agreements, invoicing, payments, and reconciliation are organized and automated, you reduce diligence friction, lower perceived risk, and strengthen your negotiating position.

Why the market shifted so fast

The accounting industry isn’t just evolving; it's transforming, compressing years of change into a short window.

Shein crystallized this shift during a session of Anchor’s Prep Your Firm webinar series, focused on the investor landscape in 2026:

“There’s been more change in the accounting industry over the last five years than in the previous 135,” he said, and he wasn't being hyperbolic.

In the talent market alone, the profession is facing a real squeeze. The AICPA reported a 6.6% drop in accounting degrees from the 2022–2023 school year to 2023–2024, driven largely by a steep decline in master’s programs.

Technology is also forcing the pace. Research from Thomson Reuters shows professionals increasingly expect AI to meaningfully reshape how work gets done, and that shift is already underway.

Meanwhile, consolidation is no longer theoretical. Deals like the Baker Tilly and Moss Adams transaction, valued at about $7 billion, underline just how quickly firm ownership structures and growth strategies are changing.

When owners step into a firm sale conversation, those big shifts usually fall into three very practical areas.

First, succession is now a valuation issue, not just a planning issue. Buyers want confidence that client relationships will transfer smoothly, especially when retirement timelines overlap.

Second, capacity is tight, particularly at the experienced level, making it harder to commit to continuity without investing in delivery and leadership depth.

Third, buyers are attracted to the stability of the work. Accounting is not discretionary in most markets, and that matters when capital is deciding where to go.

Shein put it plainly: “May you live in interesting times.”

But for firm owners, “interesting” can be an opportunity or a source of chaos. The difference is preparation and understanding how buyers will evaluate what you built.

How buyers value your firm, beyond the multiple

Most owners ask, “What multiple can I get?” Buyers ask, “What can go wrong after the owner steps back?”

That shift in perspective explains why two firms with the same revenue can see very different offers. Buyers are underwriting retention and continuity. They want confidence that clients and staff will stay and that service quality won’t dip during the transition.

Shein described accounting as a “must-have service, not a nice-to-have service.” That’s why buyers show up. But buyers still discount risk when the firm is overly dependent on a single partner, relationship manager, or rainmaker.

This is also why platforms often pay more than individual buyers. Larger groups believe they can improve operations through a repeatable playbook: expand service lines, invest in recruiting, adopt better tech and workflows, and apply scale. If they believe they can do that without breaking delivery, they pay for the future, not just the past.

The part most owners miss is what Shein called “valuation arbitrage.” Smaller firms often trade at lower multiples than larger platforms, so buyers can buy at one price, build scale, then revalue the combined business at a higher multiple.

You don’t need to love that dynamic, but you do need to understand it, because it drives deal structure and negotiation leverage.

The four buyer paths, and what you trade to take each one

IA good sale isn’t just a high price. It’s a good fit between your priorities and the buyer’s operating model. In the webinar session, Shein walked through the landscape and the tradeoffs owners should expect.

Traditional CPA firm acquisition

This is the classic route: a larger firm buys yours and integrates it. It can be a clean solution when you want a simple handoff and a stable home for clients and staff.

The tradeoff is usually flexibility. As Shein explained, the acquired firm is often “subsumed” into the larger firm. That can mean mandated systems and policies, with very little room to preserve how you run the business. These deals can work well, but they tend to be most effective when you’re comfortable relinquishing control in exchange for simplicity.

Private equity-backed platform

Private equity tends to focus on larger firms as the initial “platform,” then grows via acquisitions. If you fit the profile, there may be greater flexibility in structure, including equity rollover and growth capital.

The tradeoff is governance and, at times, pace. Shein noted that in many transactions, the private equity partner controls the board and may influence operations to varying degrees. Even when the partner is hands-off, the incentives differ from those in a traditional partner deal.

Culture and client perception can also matter more than people expect. You may not feel it internally, but clients can react to any shift in how the firm communicates, prices, or staffs their work. That is a diligence topic, not a vibes topic.

Individual CPA buyer

This is often a successor buyer who finances the purchase (sometimes through SBA-backed lending). It can be a strong continuity story when the match is right.

The tradeoff is between economics and growth capacity. An individual buyer has capital limits that typically constrain valuation, structure options, and post-close investment.

Alliance or operating partner model

There are also models that are neither traditional PE funds nor traditional CPA firm acquisitions. In the webinar, Shein described Franklin Alliance as an operating company model designed to preserve leadership control and culture while adding resources.

One line that captures how these groups position themselves: “We don’t purport to know how to run their firm better than they do.” Shein said firm leaders keep day-to-day control, with the partner providing support across recruiting, technology, growth, and acquisitions.

The tradeoff here is not “good vs bad.” It’s clarity. You still need to verify governance, mandatory changes, economics, and what control looks like in writing. Some partners market autonomy, then enforce integration through policy. Your job is to separate the pitch from the contract.

Before you go further, decide what matters most to you. High cash at close, maximum total dollars, keeping control, protecting culture, preserving brand, upside through equity, and timeline speed do not all live in the same deal.

The common trap: selling after you already stepped back

If there’s one point that should shape your timing, it’s this: the later you sell, the more your payout can depend on things you no longer control.

Shein described a scenario many owners recognize. If you wait until you’re ready to retire, a buyer may worry about relationship risk. The result is often less cash up front and more deferred payment tied to future collections. In the worst case, you’re no longer running service delivery, but your payout depends on service quality and retention.

This is why earlier planning matters. The goal isn’t to sell sooner for the sake of it. The goal is to sell when your firm is set up to operate without you as the glue, so the buyer pays for stability rather than discounting for uncertainty.

The right transition is one in which client relationships move smoothly, leaders remain accountable, and the economics don’t hinge on hope.

What to do before you talk to buyers

You don’t need a perfect firm to sell. You do need a firm that a buyer can trust after the handoff.

Start with three basics:

- Know your revenue story. Revenue by service line, client segment, and top client concentration. Not for vanity, for risk.

- Reduce owner dependency. Build a relationship transition plan, even if you plan to stay for years.

- Make operations predictable. Buyers pay for repeatability. Chaos creates discounts, holdbacks, and earnouts.

If you only do one thing, make the firm less dependent on you personally. That change shows up everywhere: valuation, structure, and the percentage of the deal paid at close.

Due diligence checklist: Questions to ask before you sign anything

Use this to keep conversations grounded and comparable across buyers. You can copy and paste it into your notes for every call.

Buyer fit and proof

- Have you acquired or partnered with firms of my size and with a service mix similar to mine?

- Can I speak with 2–3 owners you have acquired or partnered with in the last 12 months?

- What percentage of partners typically stay, and for how long?

Control and governance

- Who controls day-to-day operations after close?

- What decisions require approval (pricing, staffing model, client acceptance, tech stack)?

- What does the board look like, and who has voting control?

Deal structure and payout risk

- How much is paid at close vs deferred?

- What are earnout terms tied to (collections, retention, EBITDA)?

- If performance drops for reasons outside my control, what happens to deferred payments?

- Are there holdbacks, clawbacks, or post-close adjustments?

Equity rollover (if offered)

- What exactly do I own (common, preferred, options)?

- What is the expected liquidity path, and what has it historically looked like?

- What happens to my equity if I step back earlier than planned?

- What preferences or protections sit above my equity?

Operations and integration

- What changes are mandatory in the first 90 days?

- Will we be required to change our tech stack, workflows, or client communication?

- What shared services do you provide (billing ops, HR, recruiting, finance)?

- How do you protect service quality during transition?

Client strategy and pricing

- Will you require minimum fees or force clients to prune?

- What is your approach to pricing changes and packaging?

- How do you handle clients who push back on process changes?

People and culture

- What happens to my team's compensation and incentives?

- What is your remote or hybrid policy?

- What is your plan to retain key staff through the transition?

Growth resources

- What recruiting support is funded and active, not just planned?

- What technology support is included, and who leads implementation?

- If acquisitions are part of the plan, who sources them and who runs integration?

Make the handoff easy for the next owner

If you take one thing away from this framework, let it be this: buyers don’t just buy your revenue. They buy confidence. Confidence that client relationships will transfer, that your team can deliver without heroics, and that the numbers are clean enough to trust on day one.

That last piece is where many firm sales get unnecessarily messy. When billing is inconsistent, agreements live in email threads, invoices are rebuilt by hand, and receivables linger, buyers see risk. Risk becomes deal friction. Friction becomes holdbacks, earnouts, and longer transitions than you planned.

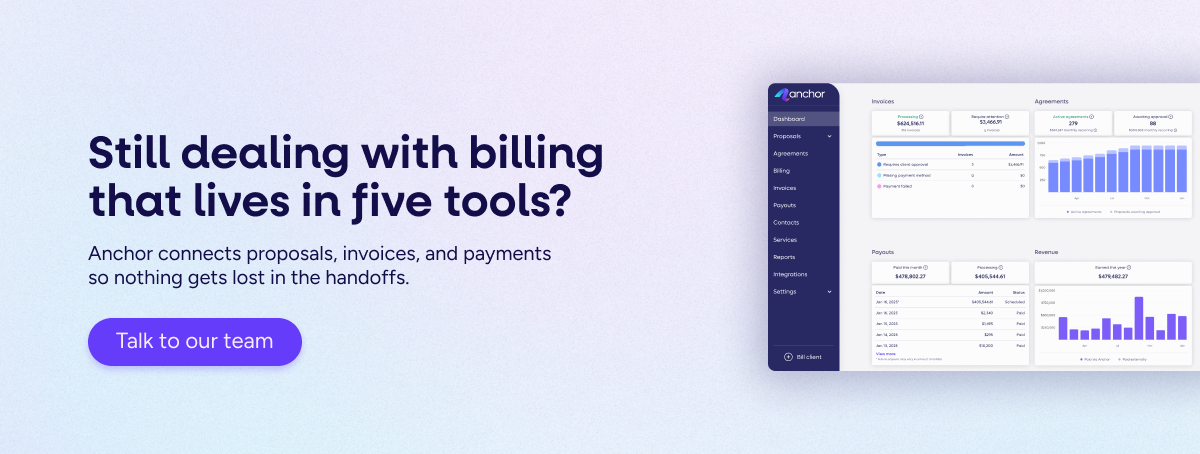

Anchor helps remove that friction by making the “work to cash” flow predictable and visible. Proposals and engagement terms are captured upfront. Invoices trigger automatically from signed agreements and billing schedules. Payments run as you set them up, so you are not relying on memory or follow-ups to get paid. Amendments are clean when scope changes. Reconciliation remains tight because payments sync and reconcile with your accounting system.

The result is simple: fewer loose ends, fewer surprises, and a firm that looks well-run the moment a buyer opens the books. One less thing to worry about now, and one more thing that can strengthen your position when the deal comes.

Want to see what that looks like in practice? Learn more about Anchor and how firms use it to turn billing, payments, and client agreements into a connected, automated system.